| Рубрикатор |  |

|

| Все новости |  |

World News | |

|

Emphasis shifts to fibre to the home

| 10 июля 2009 |

Ovum’s new broadband forecasts show a steep increase in fibre to the home/building (FTTH/B) over the forecast period, brought on by increasing deployments of next-generation access (NGA) broadband and, in some cases, significant government investment.

After literally decades of R&D investment, and specification and product development, the time for the access-fibre vendor is finally coming. However, there is always a victim in such transitions, and in this case that is DSL (ADSL in particular), as the worldwide market grinds to a halt and even goes into decline in a number of countries.

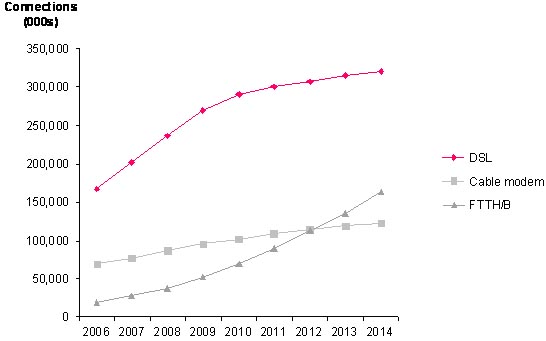

In countries such as Korea and Japan , the rapid take-up of FTTH/B and subsequent decline of ADSL technologies is nothing new. However, this network evolution is now spreading outside of Asia, and a number of western countries will start to see a rapid increase in FTTH/B and thus a decline in ADSL over the next couple of years. Most notable examples are the US , Sweden , Denmark , Finland and the Netherlands . Figure 1 (attached) depicts the ‘global residential fixed broadband access forecasts 2006 – 2014’.

Access-fibre deployment is not just confined to ‘developed countries’. A number of emerging markets such as China and Malaysia also have very ambitious FTTH/B projects. “Even if we take into account an element of government and vendor hype for these markets, Ovum still forecasts a rapid take-up of advanced broadband services in those countries”, Michael Philpott, Practice Leader of Ovum’s Consumer team. This take-up of next-generation access technologies such as FTTH and FTTB will see traditional DSL technologies saturate at around 320 million lines in the residential market by 2014, with FTTH/B still growing fast at over 160 million lines by the end of the same year. In Asia-Pacific the move to FTTH/B will be even more pronounced, with FTTH/B connections overtaking DSL to be the leading technology in 2014.

It’s not all bad news for DSL vendors

Although the worldwide market for at least ADSL technology will slow over the next five years, there are still significant opportunities for DSL vendors. Not all countries have yet announced FTTH/B initiatives and so will see significant growth in DSL over Ovum’s forecast period. “Eastern Europe, South and Central America, and Middle East and Africa will still be good growth regions for DSL operators, and thus vendors, for some years to come”, adds Mr Philpott, based in London .

Secondly, not all NGA developments are pure FTTH/B. A number, such as Japan, are actually a good mix of NGA technologies, with the advanced DSL technology VDSL2 often being used in the final few hundred meters to connect apartments and individual homes to the fibre network. Other NGA developments, such as in Belgium and the UK, will be predominantly fibre to the cabinet and then again VDSL2 in the final mile. Such NGA deployments are actually good news for DSL-based vendors as they signify the upgrade of millions of homes from ADSL line cards located in local exchanges to VDSL line cards located in street cabinets.

Thirdly, although worldwide growth will come to a standstill, there will still be over 360 million DSL lines (including business lines) in operation in 2014, with maintenance contracts running for many years to come beyond that. In Asia-Pacific however DSL connections peak in 2011.

Mobile broadband also applies pressure

The migration to FTTH/B is not the only phenomenon to stall DSL growth. By the end of 2014 worldwide consumer fixed broadband penetration will have reached only 34% of households. In theory there should therefore be plenty of growth opportunity for all fixed broadband technologies including FTTH/B. However, a large percentage of these remaining households do not have a fixed line, and whereas at one time it would have been assumed that investment in broadband would have pushed fixed lines out further, with mobile broadband devices and services becoming more readily available and affordable this will no longer be the case – at least in the medium term.

Mobile broadband has in effect set a lower ceiling for fixed broadband than what would have been predicted only 12 months ago. Whether this ceiling is permanent or not is yet to be seen. Although mobile broadband impacts fixed broadband in emerging markets more, it is not completely restricted to such countries. Western Europe , Austria , Finland, Italy and the Netherlands will all saturate at 65% of households or lower.

Global residential fixed broadband access forecasts, 2006–14

Figure 1: Global Residential Broadband Access Forecasts, 2006-14. Source: Ovum

Читайте также:

Четверть американских компаний не имеют страховки от киберугроз

На выставке "Связь" завод Инкаб анонсирует партнерские проекты

Тенденции развития ультраширокополосного доступа в интернет

Отечественный производитель пробует рынок

Аналитики сформулировали требования к сетям беспроводной связи

Оставить свой комментарий:

Комментарии по материалу

Данный материал еще не комментировался.